Gold has long been viewed as a timeless store of value, often rising in popularity when economic uncertainty or inflation concerns dominate the headlines. But what role should it play in an investment portfolio? While some investors see gold as a hedge against inflation or market volatility, others question its effectiveness compared to stocks and bonds. Striking the right balance is less about chasing short-term trends and more about understanding how gold interacts with other types of investments, and what level of allocation—if any—fits into an everyday investor’s investment strategy.

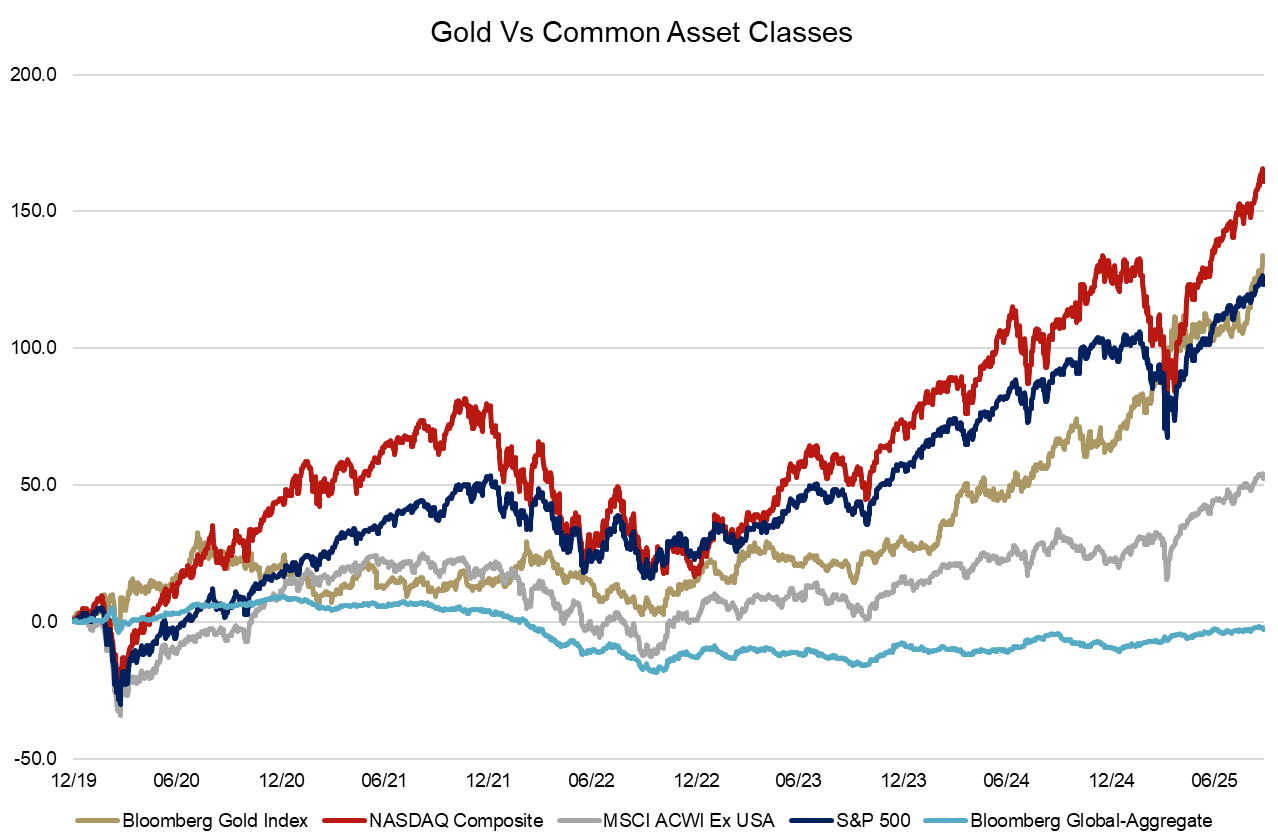

Gold prices have surged in recent years.

Central banks have been major buyers of gold in recent years, which has helped push prices higher. Many have added to their reserves to strengthen financial stability and guard against geopolitical and inflation risks. This steady, large-scale demand from central banks has provided a strong underpinning for gold prices, over and above typical investor flows.

Another explanation for gold’s recent strength is shifting investor sentiment amid rising inflation concerns and expansive policy measures. With interest rates expected to continue their decline and cash offering less appeal, gold is increasingly regarded as a safe-haven alternative. But does gold truly deserve its reputation as a “safe” asset in a portfolio?

Evaluating Gold’s Role in Investment Portfolios

As we have discussed in previous blog posts, every asset class included in a portfolio should address the following concerns:

- Are total portfolio returns enhanced?

- Has diversification improved?

The first question has a straightforward answer: no. Gold has not consistently provided investors with favorable risk-adjusted returns. Unlike stocks or bonds, commodities generate no income or earnings; their value depends solely on price appreciation. Gold’s historical performance has also been underwhelming—since 1970, gold has posted positive returns in only about 60% of calendar years, compared with roughly 80% for the S&P 500. Investors expecting gold to serve as a consistent safe haven may be left disappointed.

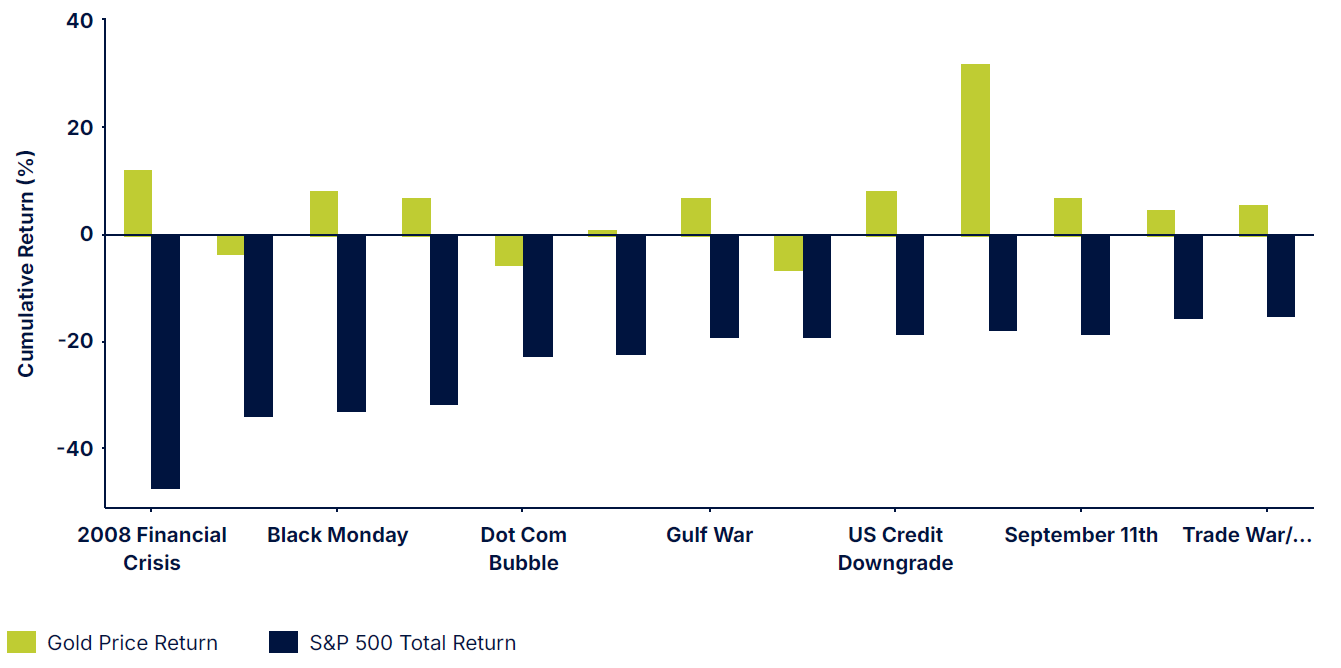

The answer to the latter question is more nuanced and widely discussed among investment professionals, but data does show that gold tends to increase in value when volatility spikes. When market volatility jumps, gold usually holds up better than stocks. On average, gold beats the S&P 500 by about 1% in weeks when the VIX (a popular measure of the stock market’s expectation of volatility) climbs. Bigger spikes make the difference even larger — around 3% when volatility jumps 20%, and over 5% when it surges 50% or more.

Sources: DFA, Blackrock, State Street

Does gold reliably defend against inflation?

High Inflation (>5%)

During periods of high inflation, gold has delivered average annual returns of around 15%, substantially outpacing inflation.

However, this performance has been uneven, with some high-inflation years seeing declines in gold prices.

Moderate Inflation (2-5%)

Gold has produced average annual returns of about 6% during periods of moderate inflation, modestly outpacing inflation but with considerable variability.

Low Inflation (<2%)

In low-inflation environments, gold has averaged annual returns of roughly 4%—positive, but often trailing equities.

Stagflation Scenarios

Gold has historically shone during stagflation (periods of high inflation paired with low economic growth), averaging annual returns of more than 20%.

Instead of thinking of gold as a perfect shield against rising prices, it’s more useful to see it as a financial asset that reacts to the broader economic landscape, including factors such as interest rates, currency stability, and long-term inflation expectations.

In conclusion, it should come as little surprise that gold is not a “be-all, end-all” asset class. Its long-term returns have lagged equities, and its volatility often exceeds that of bonds. What it has shown, however, is value as a portfolio diversifier.

Gold tends to behave differently from equities and bonds, particularly during periods of market stress or heightened volatility, helping to smooth portfolio performance and reduce overall risk. For investors seeking to strengthen portfolio resilience, a modest allocation to gold may provide this stabilizing benefit without relying on it as a primary source of returns.